UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy

Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrant ý | ||

Filed by a Party other than the Registrant o |

||

Check the appropriate box: |

||

o |

Preliminary Proxy Statement |

|

o |

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

|

o |

Definitive Proxy Statement |

|

ý |

Definitive Additional Materials |

|

o |

Soliciting Material under §240.14a-12 |

|

| MGP Ingredients, Inc. | ||||

|

(Name of Registrant as Specified In Its Charter) |

||||

|

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) |

||||

Payment of Filing Fee (Check the appropriate box): |

||||

ý |

No fee required. |

|||

o |

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

|||

| (1) | Title of each class of securities to which transaction applies: |

|||

| (2) | Aggregate number of securities to which transaction applies: |

|||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

|||

| (4) | Proposed maximum aggregate value of transaction: |

|||

| (5) | Total fee paid: |

|||

o |

Fee paid previously with preliminary materials. |

|||

o |

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

|||

(1) |

Amount Previously Paid: |

|||

| (2) | Form, Schedule or Registration Statement No.: |

|||

| (3) | Filing Party: |

|||

| (4) | Date Filed: |

|||

On July 12, 2013, the independent directors of MGP Ingredients, Inc. (the "Company") issued an open letter to the Company's stockholders, a copy of which is filed herewith as Exhibit 1. The following persons are deemed "Participants" in the solicitation of proxies in connection with the information filed herewith by virtue of their position as directors of the Company: John E. Byom, Michael Braude, Cloud L. Cray, Gary Gradinger, Linda E. Miller, Timothy W. Newkirk, Daryl R. Schaller, Karen Seaberg, and John R. Speirs. Timothy W. Newkirk and Donald P. Tracy are also a "Participant" in the solicitation by virtue of their position as executive officers of the Company.

Exhibit 1

July 12, 2013

Dear Fellow Stockholder:

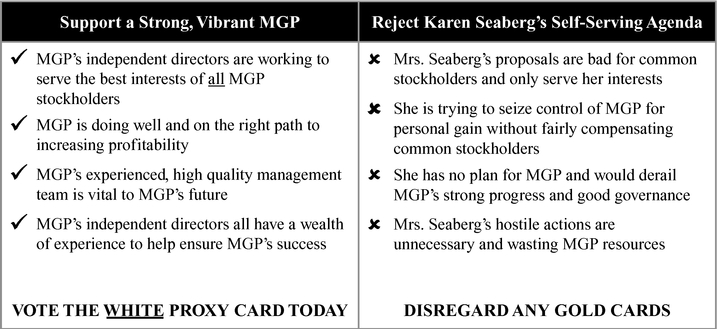

You have an important decision to make about the future of MGP. The decision is clear: support MGP's continued strong progress as a public company focused on the interests of all stockholders OR allow Karen Seaberg through her influence over the Cray Group to use MGP as her personal empire at the expense of common stockholders like you.

YOUR INDEPENDENT DIRECTORS ARE ACTING IN THE BEST INTERESTS

OF ALL MGP STOCKHOLDERS

As at every public company, the Board of Directors has a fiduciary duty to serve the best interests of all stockholders. We, the six independent directors, take our duties very seriously. Based on our average tenure of more than 12 years on MGP's Board and our extensive collective business experience, we have a deep understanding of MGP's challenges and opportunities. Along with MGP's talented management team, we are working hard to ensure MGP continues to increase profitability and stockholder value.

Our independence as directors is especially critical given the Cray family's dominant ownership in MGP. They are beneficial owners of 92% of MGP's preferred stock and 27.5% of the common stock. Through their preferred stock ownership, the family can elect five of the nine directors on the Board. Two family members already serve on the Board.

1

Prior generations, including Cloud L. Cray, Sr., MGP's founder, and his sons, Cloud L. "Bud" Cray, Jr. and Richard Cray, helped MGP grow during its early years, publicly listing it in 1988. Many of us worked with Cloud, Bud and Richard when they were leading the Company, and we respected their decision years ago to professionalize the management of the Company and ensure their own family voting processes would represent the interests of all stockholders, not just the Cray family.

Unfortunately, Cloud's granddaughter, Mrs. Karen Seaberg (already a member of MGP's Board), is now trying to undo their hard work and good intentions. Through her hostile proxy contest, she is attempting to seize control of MGP for her own benefit at the expense of common stockholders like you.

All of MGP's independent directors (including those of us who were previously elected by the Cray family) strongly oppose Mrs. Seaberg's self-serving agenda.

MRS. SEABERG IS ATTEMPTING TO SEIZE CONTROL OF MGP FOR PERSONAL GAIN WITHOUT FAIRLY COMPENSATING COMMON STOCKHOLDERS

Mrs. Seaberg's proposals and nominations would clear a path to her asserting full dominance over MGP, effectively turning MGP into a quasi-private company without compensating common stockholders.

2

Mrs. Seaberg's proxy contest is costly and unnecessary. As MGP directors, Mrs. Seaberg and her father, Bud (also an MGP director), had ample opportunities to voice any concerns with MGP and advocate for change within the established structure of the Board. Instead, after voting in favor MGP's nominees and proposals, they abruptly revoked their votes the night before the Annual Meeting of Stockholders (May 23, 2013) and launched a hostile proxy battle, which is usually an avenue taken by stockholders with no boardroom presence.

MGP IS ON THE RIGHT PATH TO DELIVERING SIGNIFICANT, SUSTAINABLE STOCKHOLDER VALUE—DON'T LET MRS. SEABERG DERAIL MGP'S PROGRESS

MGP is executing a carefully designed plan to grow profits and deliver long-term value to all stockholders. To mitigate the negative impact of the significant commodity volatility on the business and generate greater cash flow, our Board and management team have refocused MGP on a higher value sales mix, developed a more effective supply chain and increased productivity across our asset base.

By implementing this strategy, MGP is well positioned to capitalize on the strong growth of the distilled spirits market, particularly the surge in popularity among high-end and super-premium whiskeys. In 2012, U.S. whiskey sales increased by 3.6%—higher than growth for vodka, gin and tequila and the largest such increase in 30 years(1). Our focus on expanding our presence in higher margin businesses like premium distilled spirits, as well as nutritional health innovations, while also ensuring we remain a low cost white goods producer is generating real results:

3

With respect to Mrs. Seaberg, we do not believe she has the experience or business acumen to lead MGP. Beyond her MGP Board membership, the extent of her business experience has been working as an executive travel agent, local restaurateur and being involved in community charity organizations.

REVIEW OF STRATEGIC ALTERNATIVES INCLUDES WIDE RANGE OF OPTIONS

We are confident that our strategy will continue to drive revenue and cash flow generation leading to higher profits and value for all stockholders. However, one constant in the business world is the need to continually evolve. To ensure we are exploring all avenues to maximizing value, the independent members of the Board are conducting a strategic review of alternatives. Contrary to Mrs. Seaberg's misleading statements, this does not necessarily mean the Company will be sold. The Board is reviewing a wide range of alternatives. The process may take several months to complete, and it is critical that the Company continue to progress and execute at the highest levels during this time.

WE ARE COMMITTED TO ATCHISON AND OTHER COMMUNITIES

WHERE WE LIVE AND WORK

Through her various interviews with local media, Mrs. Seaberg claims MGP is not committed to the communities where it operates. That is a blatant misrepresentation of the facts. Several directors and most of MGP's management team live in Atchison. The MGP team works hard to support the communities where we live and work, whether through donations to local charities, engagement with community leaders and civic causes, or growth of the business itself. Under our stewardship, dating back to before Mrs. Seaberg joined the Board, MGP has invested over $27 million into expanding its facilities in Atchison. This multi-year investment, which included the construction of a new Corporate Office and Technical Innovation Center, added significantly to the local economy and reflects our commitment to the community. For as long as we remain directors, we plan to keep MGP headquartered in Atchison.

MRS. SEABERG HAS NO PLAN AND IS MISLEADING STOCKHOLDERS

Mrs. Seaberg has not offered an alternative plan other than asserting dominance over MGP at the expense of your interests and terminating management who dare to act independently of her. She desires control for control's sake. Mrs. Seaberg is relying on incomplete and inaccurate statements we believe to mislead stockholders.

4

health. Subsequent changes to the Trust by Mrs. Seaberg are further evidence of her attempt to manipulate governance of the Company to her advantage.

RETURN YOUR WHITE CARD TO SUPPORT YOUR INDEPENDENT BOARD AND

MGP'S STRONG PROGRESS

Mrs. Seaberg appears to be trying to steamroll over MGP's stockholders in a self-serving effort to purge disloyalty to her and reassert family control. However, as you know, the duty of any public company Board is to serve the best interests of all stockholders. That is our commitment to you, and we take it seriously. We appreciate your support of a strong, independent Board at MGP and the progress we are making delivering value to all stockholders.

5

You may have received a WHITE proxy card from the Company related to our May 23, 2013 annual meeting, which was adjourned and will be rescheduled in due course. If you voted that WHITE card already, you do not need to take any further action. If you have not voted the WHITE card yet, we encourage you to do so today.

Thank you again for your support,

|

John R. Speirs Chairman |

Michael Braude Director |

John E. Byom Director |

Gary Gradinger Director |

|||

|

Linda E. Miller Director |

Daryl R. Schaller, Ph.D. Director |

|||||

The Independent Directors of the Board

If

you have questions about how to vote your shares, or need additional assistance,

please contact the firm assisting us in the solicitation of proxy votes:

Innisfree M&A Incorporated

Stockholders Call Toll-Free: (888) 750-5834

Banks and Brokers Call: (212) 750-5833

IMPORTANT

Vote the White Proxy Card today!

FORWARD-LOOKING STATEMENTS SAFE HARBOR

This letter contains forward-looking statements as well as historical information. Forward-looking statements are usually identified by or are associated with such words as "intend," "plan," "believe," "estimate," "expect," "anticipate," "hopeful," "should," "may," "will," "could," "encouraged," "opportunities," "potential" and/or the negatives of these terms or variations of them or similar terminology. They reflect management's current beliefs and estimates of future economic circumstances, industry conditions, Company performance and financial results and are not guarantees of future performance. All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement. Investors should not place undue reliance upon forward-looking statements and the Company undertakes no obligation to publicly update or revise any forward-looking statements. Important factors that could cause actual results to differ materially from our expectations include, among others: (i) disruptions in operations at our Atchison facility or Indiana Distillery, (ii) the availability and cost of grain and fluctuations in energy costs, (iii) the effectiveness of our

6

hedging strategy, (iv) the competitive environment and related market conditions, (v) the ability to effectively pass raw material price increases on to customers, (vi) the viability of the Illinois Corn Processing, LLC ("ICP") joint venture and its ability to obtain financing, (vii) our ability to maintain compliance with all applicable loan agreement covenants, (viii) our ability to realize operating efficiencies, (ix) actions of governments, (x) and consumer tastes and preferences. For further information on these and other risks and uncertainties that may affect our business, including risks specific to our Distillery and Ingredient segments, see Item 1A. Risk Factors of our Annual Report on Form 10-K for the year ended December 31, 2012.

IMPORTANT ADDITIONAL INFORMATION

MGP Ingredients, Inc., its directors, and certain of its officers are participants in the solicitation of proxies from MGP stockholders in connection with the Company's 2013 Annual Meeting of Stockholders. Important information concerning the identity and interests of these persons is available in the definitive proxy statement that MGP filed with the SEC on April 11, 2013 as subsequently supplemented, including the proxy supplement dated July 12, 2013.

The definitive proxy statement, any other relevant documents and other materials filed with the SEC concerning MGP are available free of charge at www.sec.gov and www.mgpingredients.com. Stockholders should carefully read the definitive proxy statement, including supplements thereto, before making any voting decision.

7