|

MGP Ingredients, Inc.

Cray Business Plaza

100 Commercial St., P.O. Box 130

Atchison, Kansas 66002-0130

800.255.0302

www.mgpingredients.com

|

October 15, 2012

Brad Skinner

Senior Assistant Chief Accountant

Securities and Exchange Commission

Washington, D.C. 20549

Re: MGP Ingredients, Inc.

Form 10-K for the Transition Period from July 1, 2011 to December 31, 2011

Filed March 13, 2012

File No. 000-17196

Dear Mr. Skinner:

This is in response to your letter dated September 26, 2012 in respect to MGP Ingredients, Inc.’s (the Company) annual report on Form 10-K for the transition period ended December 31, 2011. We have responded to your comments, which we have underlined below. We hope this letter adequately addresses your questions.

Form 10-K For the Transition Period from July 1, 2011 to December 31, 2011

Note 1: Nature of Operations and Summary of Significant Accounting Policies

Out-of-period Adjustments, page 87

|

1.

|

We note that during the second quarter of fiscal 2010 you discovered certain transactions recorded in the prior fiscal year had been either duplicated or otherwise erroneously recorded in accounts payable balance. Consequently, you determined certain recorded amounts were not owed and adjusted the accounts payable balance in the second quarter of fiscal 2010 to correct the accounting records. You further disclose that the impact of the correcting adjustment increased reported pretax income for the second quarter of fiscal 2010 by approximately $1,351 thousands. Please explain to us in greater detail how you accounted for this correction of error, stating the applicable U.S. GAAP and addressing FASB ASC 250-10-45-23.

|

During the second quarter of fiscal 2010, the Company became aware of instances of duplicated accounts payable accruals. The original accruals that had been automatically recorded by the system were later duplicated by a manual accrual established at the time of goods receipt.

Based on guidance under ASC 250-10-45-271, the Company assessed the impact of the out-of-period errors on both reported earnings for fiscal 2009, when substantially all of the error occurred, and on estimated annual net income for fiscal 2010. In fiscal 2009 we had implemented major changes to our business and, as a result, had recorded large special charges.In addition, we evaluated the effect of the error on actual 2010 net income and on the trend of the Company’s earnings prior to filing our fiscal 2010 Form 10-K. Changes made in fiscal 2009 enabled us to get back to essentially a breakeven level in fiscal 20102.

To correct the error, the Company reversed the duplicate payables of $1.351 million (with the offsetting credit recorded to operating income) in second quarter fiscal 2010. Actual results reported for the second quarter fiscal 2010 included income to-date before taxes of $3.9 million, including the reversal of the duplicate payables. Net income was increased by a change in tax law that allowed us to carry back and realize an additional $4.6 million of NOLs, which we disclosed.

Rising commodity prices then depressed earnings in the second half of fiscal 2010 to essentially a breakeven level, which was a significant improvement versus the large losses of the previous fiscal year.

We determined that the correction of this error did not materially misstate fiscal 2009 or 2010 or any previous period. The basis for our decision was a materiality assessment, which is provided in 3 below. Because we concluded that this correction was immaterial, a restatement (under FASB ASC 250-10-45-23) of the fiscal 2009 or 2010 financial statements was not considered necessary. Our accounting treatment of this followed the guidance for correction of an immaterial error.

Our earnings since fiscal 2007, last five years, are listed and charted as follows (in millions):

2007 $17.6

2008 ($11.7)

2009 ($69.1)

2010 $8.7 (includes $1.351 error correction and tax benefit of $4.768)

2011 ($1.3)

2011 $10.6 (six-month transition period to new 12/31 yearend)

____________________

1 ASC 250-10-45-27 “In determining materiality for the purpose of reporting the correction of an error, amounts shall be related to the estimated income for the full fiscal year and also to the effect on the trend of earnings. Changes that are material with respect to an interim period but not material with respect to the estimated income for the full fiscal year or to the trend of earnings shall be separately disclosed in the interim period.”

2 During fiscal 2009 the Company was negatively impacted by overall economic conditions and laid off approximately 50% of its work force, including a number of corporate staff positions. This situation contributed to these errors being made by individuals with limited experience in receiving and recording goods. The Company worked with great care to remedy this situation in 2010. We hired additional highly-qualified finance team members to facilitate more extensive monitoring of accruals and also converted to a new ERP system with solid inherent automated controls that are tested regularly as part of the overall review of our system of internal controls. As an integral part of the conversion to the new system, procurement staff members were extensively trained in the appropriate receiving and recording of goods and a training plan for new hires was executed.

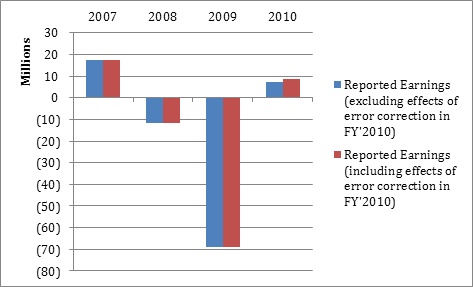

The chart below compares reported earnings, excluding effects of the error correction in fiscal 2010, for the years affected (including de minimis years) to reported earnings, including effects of the error correction in fiscal 2010, for the years affected (including de minimis years). We concluded that the comparison yields an immaterial variance to reported earnings in fiscal 2010:

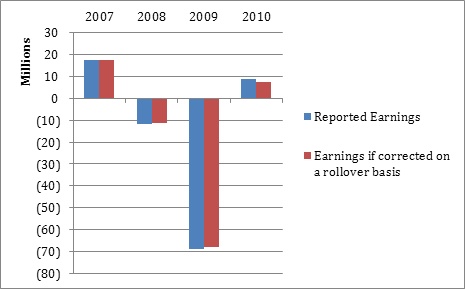

The chart below compares reported earnings for the years affected (including de minimis years) to reported earnings for the years affected (including de minimis years), had the errors been corrected on a rollover basis. We concluded that a rollover error correction compared to the correction in fiscal 2010 yields immaterial variances in years affected.

As illustrated above, there has been no recent trend in company earnings. The earnings pattern reflects several factors but most notably—

|

a.

|

Highly fluctuating prices for fuel grade alcohol prior to fiscal 2009 when we substantially reduced our exposure to this product

|

|

b.

|

Highly volatile commodity prices for key inputs in our manufacturing process primarily corn, natural gas and to a lesser extent wheat.

|

|

c.

|

Overall difficult economic conditions during much of the past five years which necessitated the restructuring of our business in fiscal 2009.

|

We do not provide any earnings guidance and do not have any analysts who try to estimate our earnings. Thus, there were no street expectations of earnings for any period.

|

2.

|

Also in this regard, please provide us with all disclosures required under paragraphs 7 – 9 of ASC 250-10-50.

|

As stated in response to comment 1, the Company concluded this matter was immaterial and that a restatement was not considered necessary. Because the financial statements were not restated, the required disclosures related to restatements (FASB ASC 250-10-50 (paragraphs 7-9) were determined not to be warranted. Our related 10-Q and 10-K disclosures for second quarter and yearend fiscal 2010, respectively, follow below:

|

a.

|

Second quarter fiscal 2010 disclosure ($ in millions):

|

Out-of-Period Adjustments

Out-of-period adjustments are detailed below. Management does not believe the impact of these out of period adjustments materially impact the fair presentation of the Company’s operating results or financial condition for the periods impacted.

Accounts Payable. During the second quarter of fiscal 2010 management performed a detailed analysis of accounts that were either duplicated or otherwise erroneously recorded. After analysis, the Company determined certain recorded amounts were not owed and adjusted the accounts payable balance in the second quarter to correct this situation. The impact of the correcting adjustment increased reported pretax income in the second quarter of fiscal 2010 by approximately $1,351. Cost of sales was favorably impacted by $733, and the result of equity in earnings (loss) of joint ventures was improved by $618.

|

b.

|

Yearend fiscal 2010 disclosure ($ in millions):

|

Out-of-period Adjustments

During the second quarter of fiscal 2010, management performed a detailed analysis of the accounts payable balance. The analysis indicated certain transactions recorded in the prior fiscal year had been either duplicated or otherwise erroneously recorded. After analysis, the Company determined certain recorded amounts were not owed and adjusted the accounts payable balance in the second quarter of fiscal 2010 to correct the accounting records.

The impact of the correcting adjustment increased reported pretax income for the second quarter of fiscal 2010 by approximately $1,351. Cost of sales was favorably impacted by $733, and other income was improved by $618 in the second quarter of fiscal 2010. Management does not believe the impact of this out-of-period adjustment materially impacts the fair presentation of the Company’s operating results or financial condition for the periods impacted.

|

3.

|

Finally, you disclose that the impact of the correcting adjustment does not materially impact the fair presentation of the Company’s operating results or financial condition for the periods impacted. Refer to SAB Topic 1M and provide us with your materiality analysis.

|

|

a.)

|

Effects of error correction on actual results at yearend fiscal 2010 ($ in millions):

|

Error Correction $1.351 (pre-tax)

Pre-tax Income $4.0

Net Income $8.7 (includes $4.768 tax benefit and error correction)

Error % of Pre-tax Income 33.78 %

Error % of Net Income 18.38 % (excludes error correction)

|

b.)

|

Effects of error correction on actual results at yearend fiscal 2009 ($ in millions):

|

Error Correction $1.351 (pre-tax)

Pre-tax Income ($81.9)

Net Income ($69.1)

Error % of Pre-tax Income 1.65 %

Error % of Net Income 1.95 %

The following table details by fiscal quarter the effects of the error correction for fiscal 2009:

| |

|

Net Income ($) |

|

|

Error ($) |

|

|

% Error |

|

| Q1 FY09 |

|

|

(17.2 |

) |

|

|

0.334 |

|

|

|

-1.94 |

% |

| Q2 FY09 |

|

|

(42.7 |

) |

|

|

0.638 |

|

|

|

-1.49 |

% |

| Q3 FY09 |

|

|

(6.2 |

) |

|

|

0.271 |

|

|

|

-4.34 |

% |

| Q4 FY09 |

|

|

(2.9 |

) |

|

|

0.108 |

|

|

|

-3.70 |

% |

| |

|

|

(69.1 |

) |

|

|

1.351 |

|

|

|

-1.95 |

% |

|

c.)

|

SAB Topic 1M Analysis:

|

The Company reviewed the qualitative factors outlined in SEC Staff Accounting Bulletin Topic 1M, which may render a quantitatively small misstatement material, and noted the following:

|

i)

|

Whether the misstatement arises from an item capable of precise measurement or whether it arises from an estimate and, if so, the degree of imprecision inherent in the estimate.

|

Response: The misstatement did not arise from an estimate. During fiscal 2009 the Company was negatively impacted by overall economic conditions and laid off approximately 50% of its work force including a number of corporate staff positions as discussed previously. This situation contributed to these errors being made by individuals with limited experience in receiving and recording goods. The Company worked with great care to remedy this situation in 2010. We hired additional highly-qualified finance team members to facilitate more extensive monitoring of accruals and also converted to a new ERP system with solid inherent automated controls that are tested regularly as part of the overall review of our system of internal controls. As an integral part of the conversion to the new system, procurement staff members were extensively trained in the appropriate receiving and recording of goods and a training plan for new hires was executed.

|

ii)

|

Whether the misstatement masks a change in earnings or other trends; hides a failure to meet analysts’ consensus expectations for the enterprise; or changes a loss into income or vice versa.

|

Response: This misstatement does not mask a change in earnings or other trends, or change a loss to income in the current period. The Company recorded a large loss in fiscal 2009. We returned to profitability in fiscal 2010. Fiscal 2010 was a turnaround year designed to return the Company to profitability. The error correction was initially evaluated during second quarter fiscal 2010 against expected earnings for the entire fiscal year of $11.4 million. Thus, the error was expected to approximate 11.3% of net income. After considering all the qualitative factors and the importance of this adjustment from an investor’s perspective, management determined that disclosure of an immaterial correction was appropriate. At the end of second quarter fiscal 2010 actual net income of about $8.5 million was trending ahead of expected forecasted earnings of $11.4 million for the entire fiscal year.

|

iii)

|

Whether the misstatement concerns a segment or other portion of the registrant's business that has been identified as playing a significant role in the registrant's operations or profitability.

|

Response: The uncorrected misstatement was related to the Company's procurement activities. Correction of the error changed the reported pretax income results for our three operating segments. The effect on fiscal 2009 was insignificant and did not distort any trends of any segment results.

For the impact of the correction of the error on second quarter and year-to-date fiscal 2010, the Company, consistent with their policy for similar items and corporate expense items, did not allocate the benefit of the correction to fiscal 2010 segment results. As such, the item is separately disclosed and does not affect fiscal 2010 segment results.

|

iv)

|

Whether the misstatement affects the registrant's compliance with regulatory requirements.

|

Response: There is no impact on the Company's compliance with regulatory requirements.

|

v)

|

Whether the misstatement affects the registrant's compliance with loan covenants or other contractual requirements.

|

Response: The Company considered potential impacts of the misstatements on compliance with loan covenants and other contractual requirements. On July 21, 2009, we entered into a $25 million, three-year credit agreement with our bank, extending until July 2012. The Company was subject to covenant compliance requirements with respect to the credit agreement. We were required to attain net income minimum cumulative thresholds at various points of the year, with the fiscal 2010 yearend minimum net income being $3.5 million. For the six months ended December 31, 2009, the Company was subject to a minimum net income requirement of $1.5 million. At December 31, 2009, we had net income of approximately $8.5 million. With or without this error correction gain on goods received but not invoiced, net income would nonetheless have well exceeded minimum debt covenant requirements. As such, this misstatement had no impact on the Company's compliance with loan covenants.

|

vi)

|

Whether the misstatement has the effect of increasing management's compensation - for example, by satisfying requirements for the award of bonuses or other forms of incentive compensation.

|

Response: The impact of the uncorrected misstatements identified in the second quarter of fiscal 2010 did not have an impact on the Company's ability to meet incentive compensation targets for the year. With respect to fiscal 2010, full disclosure of the correction was provided to the Board of Directors for consideration in fiscal 2010 potential yearend payouts. The effect of the correction was excluded from fiscal 2010 yearend payout computations.

|

vii)

|

Whether the misstatement involves concealment of an unlawful transaction.

|

Response: The misstatement did not involve the concealment of or relate to an unlawful transaction. The transactions that gave rise to the uninvoiced PO receipt gain were not purposeful. There is no known intent or motivation for any concealment.

In analyzing the materiality of the errors, the Company considered the guidance provided by the SEC, specifically the guidance provided in the Todd Hardiman, Associate Chief Accountant of the SEC Division of Corporation Finance 2006 speech before the 2006 AICPA National Conference on Current SEC and PCAOB Developments where it was stated that large errors could be deemed immaterial due to qualitative factors in certain circumstances, of which he identified two potential examples - errors in unusual breakeven years and errors in discontinued operations. We believe the conditions we experienced in fiscal 2009 and 2010 are consistent with unusual breakeven years noted in Mr. Hardiman’s comments. In fiscal 2009 we experienced a pre-tax loss of $81.9 million and essentially returned to slightly above the break-even level in fiscal 2010 when we reported $4 million of pre-tax income. If the effects of the error correction of $1.351 million and the tax benefit of $4.768 million are excluded from net income for fiscal 2010, net income would be $2.619 million: essentially breakeven. Given the break-even nature of fiscal 2010, we believe that revenues would be a more meaningful denominator to assess the error against, and the impact of the error on fiscal 2010 revenues of $202 million is less than 1%.

The Company concluded that the effect of the correction of the $1.351 million error was not material to either fiscal 2009, when substantially all of the error occurred, or to fiscal 2010, when the error was corrected and disclosed as an immaterial correction. We also concluded that the error correction did not affect the trend of earnings. We consulted currently and contemporaneously with our external auditors regarding the accounting treatment of this error correction and consensus was obtained on our conclusions.

The Company concludes that the identified misstatement lacks the qualitative factors outlined in SAB Topic 1M that would require a restatement of earnings.

The out-of-period correction in second quarter fiscal 2010 also did not introduce qualitative factors that indicated the error is material. Further, we did not identify any additional qualitative factors that would indicate the error is material when the error was reevaluated at the end of the fiscal year using actual yearend earnings.

Management thus concluded that, based on guidance in SAB 99 (including SAB Topic 1M) and ASC 250-10-45-27, the effect and impact of the misstatement identified in the second quarter of fiscal 2010 continues to be immaterial to the financial statements for all periods impacted. We have made appropriate disclosures of this error correction and believe these are appropriate and responsive to the situation we encountered and provide transparency about this matter to an investor.

Thank you for your comments. The Company acknowledges that we are responsible for the adequacy of the disclosure in the filing; that staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and that the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Please call me at 913-360-5435 or email me at don.tracy@mgpingredients.com if you have any questions about our responses or if we can provide you with any other information that will facilitate your review.

Sincerely,

/s/ Don Tracy

Don Tracy

Vice President and Chief Financial Officer