SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

___________________________

FORM 10-K

ANNUAL REPORT

PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

|

| |

(Mark One) |

X | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

|

| |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to _______

Commission file number 0-17196

MGP Ingredients, Inc.

(Exact Name of Registrant as Specified in Its Charter)

|

| |

Kansas | 45-4082531 |

(State or Other Jurisdiction | (I.R.S. Employer |

of Incorporation or Organization) | Identification No.) |

| |

100 Commercial Street, Box 130, Atchison, Kansas | 66002 |

(Address of Principal Executive Offices) | (Zip Code) |

(913) 367-1480

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

|

| |

Title of Each Class | Name of Each Exchange on Which Registered |

Common Stock, no par value | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes __ No X

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes __ No X

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No ____

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes X No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to their Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "large accelerated filer", "accelerated filer" and "smaller reporting company": in Rule 12b-2 of the Exchange Act. (Check One):

Large accelerated filer ___ Accelerated filer X Non-accelerated filer ___ Smaller reporting company ___

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ___ No X

The aggregate market value of common equity held by non-affiliates, computed by reference to the last sales price as reported by NASDAQ on June 30, 2016, was $487,505,243.

The number of shares of the registrant’s common stock, no par value ("Common Stock") outstanding as of March 3, 2017 was 16,708,742.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents are incorporated herein by reference:

| |

(1) | Portions of the MGP Ingredients, Inc. Proxy Statement for the Annual Meeting of Stockholders to be held on June 1, 2017 are incorporated by reference into Part III of this report to the extent set forth herein. |

CONTENTS PAGE

|

| | | |

| | |

| | Business | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | Consolidated Statements of Income - Years Ended December 31, 2016, 2015, and 2014 | |

| | Consolidated Statements of Comprehensive Income - Years Ended December 31, 2016, 2015, and 2014 | |

| | Consolidated Balance Sheets - December 31, 2016 and 2015 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| Item 16. | Form 10-K Summary | |

| | |

The calculation of the aggregate market value of the Common Stock held by non-affiliates is based on the assumption that affiliates include directors and executive officers. Such assumption does not constitute an admission by the Company or any director or executive officer that any director or executive officer is an affiliate of the Company.

PART I

ITEM 1. BUSINESS

MGP Ingredients, Inc. was incorporated in 2011 in Kansas, continuing a business originally founded by Cloud L. Cray, Sr. in Atchison, Kansas in 1941. The Company’s ticker symbol is MGPI. As used herein, the term "MGP," "Company," "we," "our," or "us" refers to MGP Ingredients, Inc. and its subsidiaries unless the context indicates otherwise. In this document, for any references to Note 1 through Note 18 refer to the Notes to Consolidated Financial Statements in Item 8.

AVAILABLE INFORMATION

We make available through our website (www.mgpingredients.com) under "Investors - Investor Relations," our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, special reports and other information, and amendments to those reports as soon as reasonably practicable after we electronically file or furnish such material with the Securities and Exchange Commission.

METHOD OF PRESENTATION

All amounts in this report, except for shares, par values, bushels, gallons, pounds, mmbtu, proof gallons, per share, per bushel, per gallon, per proof gallon and percentage amounts, are shown in thousands unless otherwise noted.

GENERAL INFORMATION

MGP is a leading producer and supplier of premium distilled spirits and specialty wheat protein and starch food ingredients. Distilled spirits include premium bourbon and rye whiskeys, and grain neutral spirits, including vodka and gin. MGP is also a top producer of high quality industrial alcohol for use in both food and non-food applications. Our protein and starch food ingredients provide a host of functional, nutritional and sensory benefits for a wide range of food products to serve the packaged goods industry. Our distillery products are derived from corn and other grains (including rye, barley, wheat, barley malt, and milo), and our ingredient products are derived from wheat flour. The majority of our distillery and ingredient product sales are made directly or through distributors to manufacturers and processors of finished packaged goods or to bakeries.

We are headquartered in Atchison, Kansas, where distilled alcohol products and food ingredients are produced at our production facility ("Atchison facility"). Premium spirits are also distilled and matured at our facility in Lawrenceburg and Greendale, Indiana ("Lawrenceburg facility").

INFORMATION ABOUT SEGMENTS

As of December 31, 2016, we had two reportable segments: distillery products and ingredient solutions. Additional information about our reportable segments can be found in Management’s Discussion & Analysis ("MD&A") and Note 11.

Distillery Products Segment - We process corn and other grains into food grade alcohol and distillery co-products, such as distillers feed (commonly called dried distillers grain in the industry), fuel grade alcohol, and corn oil. We also provide warehouse services, including barrel put away, barrel storage, and barrel retrieval services. We have certain contracts with customers to supply distilled products (or "distillate"), as well as certain contracts with customers to provide barreling and warehousing services. Contracts with customers may be monthly, annual, and multi-year with periodic review of pricing. Sales of fuel grade alcohol are made on the spot market. Since 2015 our distillery products segment includes some production and sales of our own branded alcohol products. During 2016, our five largest distillery products customers, combined, accounted for about 23 percent of our consolidated net sales.

Food Grade Alcohol - The majority of our distillery capacities are dedicated to the production of high quality, high purity food grade alcohol for beverage and industrial applications.

Food grade alcohol sold for beverage applications ("premium beverage alcohol") consists primarily of premium bourbon and rye whiskeys, and grain neutral spirits, including vodka and gin. Our premium bourbon is created by distilling grains, primarily corn. Our whiskey is made from fermented grain mash, including rye and corn. Our whiskeys are primarily sold as unaged new distillate, which are then aged by our customers from two to four years and are sold at various proof concentrations. Grain neutral spirits are sold in bulk quantities at various proof concentrations. Our gin is created by redistilling grain neutral spirits together with proprietary formulations of botanicals or botanical oils.

In November 2016, we acquired the George Remus® brand from Queen City Whiskey LLC. The prior owner used sourced whiskey from us to launch and successfully build the brand in a small geography. The George Remus® brand portfolio currently consists of three expressions: George Remus® Bourbon Whiskey, George Remus® Rye Whiskey, and George Remus® Limited Edition Rye Whiskey. At the time of the acquisition, distribution was limited to the states of Ohio, Kentucky and Indiana.

In March 2016, we introduced a vodka brand, Till American Wheat Vodka®, distilled using the finest Kansas wheat with initial distribution in the states of Kansas and Missouri. In October 2016, we announced that distribution was expanded to the states of Iowa and Indiana.

In July 2015, we announced our first branded alcohol product, Metze's Select, which was made available for retail sale in September 2015. Metze's Select was a limited edition Indiana Straight Bourbon Whiskey.

Food grade industrial alcohol is used as an ingredient in foods (e.g., vinegar and food flavorings), personal care products (e.g., hair sprays and hand sanitizers), cleaning solutions, pharmaceuticals, and a variety of other products. We sell food grade industrial alcohol in tank truck or rail car quantities direct to a number of industrial processors.

Distillers Feed and related Co-Products - The bulk alcohol co-products sales include distillers feed, fuel grade alcohol, and corn oil. Distillers feed is principally derived from the mash from alcohol processing operations. The mash is dried and sold primarily to processors of animal feeds as a high protein additive. We produce fuel grade alcohol as a co-product of our food grade alcohol business at our distillery in Atchison. We produce corn oil as a value added co-product through a corn oil extraction process.

Fuel grade alcohol is sold primarily for blending with gasoline to increase the octane and oxygen levels of the gasoline. As an octane enhancer, fuel grade alcohol can serve as a substitute for lead and petroleum-based octane enhancers. As an oxygenate, fuel grade alcohol has been used in gasoline to meet certain environmental regulations and laws relating to air quality by reducing carbon monoxide, hydrocarbon particulates and other toxic emissions generated from the burning of gasoline.

Warehouse Services - Customers who purchase unaged barreled whiskey distillate may, and in most cases do, also enter into separate warehouse service agreements with us for the storage of product for aging that include services for barrel put away, barrel storage and barrel retrieval. Revenue from warehousing services is recognized upon providing the service and/or over the passage of time, as in the case of storage fees.

Ingredient Solutions Segment - Our ingredient solutions segment consists primarily of specialty wheat starches, specialty wheat proteins, commodity wheat starch and commodity wheat proteins. Contracts with ingredients customers are generally price, volume, and term agreements, which are fixed for three or six month periods, with very few agreements of 12 months duration or more. During 2016, our five largest ingredient solutions customers, combined, accounted for about 11.1 percent of our consolidated net sales.

Specialty Wheat Starches - Wheat starch derived from the carbohydrate bearing portion of wheat flour. We produce a premium wheat starch powder by extracting the starch from the starch slurry, substantially free of all impurities and fibers, and then dry the starch in spray, flash or drum dryers.

A substantial portion of our premium wheat starch is altered during processing to produce certain unique specialty wheat starches designed for special applications. We sell our specialty starches on a global basis, primarily to food processors and distributors.

We market our specialty wheat starches under the trademarks Fibersym® Resistant Starch series, FiberRite® RW Resistant Starch, Pregel® Instant Starch series, and Midsol® Cook-up Starch series. They are used primarily for food applications as an ingredient in a variety of food products to affect their nutritional profile, appearance, texture, tenderness, taste, palatability, cooking temperature, stability, viscosity, binding and freeze-thaw characteristics. Important physical properties contributed by wheat starch include whiteness, clean flavor, viscosity and texture. For example, our starches are used to improve the taste and texture of cream puffs, éclairs, puddings, pie fillings, breading and batters; to improve the size, symmetry and taste of angel food cakes; to alter the viscosity of soups, sauces and gravies; to improve the freeze-thaw stability and shelf life of fruit pies and other frozen foods; to improve moisture retention in microwavable foods; and to add stability and to improve spreadability in frostings, mixes, glazes and sugar coatings.

Our wheat starches, as a whole, generally compete primarily with corn starch, which dominates the United States starch market. However, the unique characteristics of our specialty wheat starches provide a number of advantages over corn and other starches for certain baking and other end uses.

Specialty Wheat Proteins - We have developed a number of specialty wheat proteins for food applications. Specialty wheat proteins are derived from vital wheat gluten through a variety of proprietary processes which change its molecular structure. Specialty wheat proteins for food applications include products in the Arise® , Optein®, and Trutex®. Our specialty wheat proteins generally compete with other ingredients and modified proteins having similar characteristics, primarily soy proteins and other wheat proteins, with differentiation being based on factors such as functionality, price and, in the case of food applications, flavor.

Commodity Wheat Starch - As is the case with value added wheat starches, our commodity wheat starch has both food and non-food applications, but such applications are more limited than those of value added wheat starches and typically sell for a lower price in the marketplace. Commodity wheat starch competes primarily with corn starches, which dominate the marketplace and prices generally track the fluctuations in the corn starch market.

Commodity Wheat Proteins - Commodity wheat protein, or vital wheat gluten, is a free-flowing light tan powder which contains approximately 70 to 80 percent protein. When we process wheat flour to derive starch, we also derive vital wheat gluten. Vital wheat gluten is added by bakeries and food processors to baked goods, such as breads, and to pet foods, cereals, processed meats, and fish and poultry to improve the nutritional content, texture, strength, shape and volume of the product. The neutral flavor and color of vital wheat gluten also enhances the flavor and color of certain foods. The cohesiveness and elasticity of the gluten enables the dough in wheat and other high protein breads to rise and to support added ingredients, such as whole cracked grains, raisins and fibers. This allows bakers to make an array of different breads by varying the gluten content of the dough. Vital wheat gluten is also added to white breads, hot dog buns, and hamburger buns to improve the strength and cohesiveness of the product.

COMPETITIVE CONDITION

The markets in which our products are sold are competitive. Our products compete against similar products of many large and small companies. In our distillery products segment, competition is based primarily on product innovation, product characteristics, functionality, price, service and quality factors such as flavor. In our ingredient solutions segment competition is based primarily on product innovation, product characteristics, price, name, color, flavor, or other properties that affect how the ingredient is being used.

PATENTS, TRADEMARKS, AND LICENSES

We are involved in a number of patent related activities. We have filed patent applications to protect a range of inventions made in our expanding research and development efforts, including inventions relating to applications for our products. Some of these patents or licenses cover significant product formulation and processes used to manufacture our products.

RESEARCH AND DEVELOPMENT

During 2016, 2015, and 2014, we incurred $916, and $748, and $1,622 respectively, on research and development activities. Research and development activities allow us to develop products across both of our segments to respond to changing consumer trends.

SEASONALITY

Our sales are generally not seasonal.

TRANSPORTATION

Historically, our output has been transported to customers by truck and rail, most of which is provided by common carriers. We use third party transportation companies to help us manage truck and rail carriers who deliver our products to our North American customers. As of December 31, 2016, we leased 207 rail cars under operating leases.

RAW MATERIALS AND PACKAGING MATERIALS

Our principal distillery products segment raw materials are corn and other grains (including rye, barley, wheat, barley malt, and milo), which are processed into food grade alcohol and distillery co-products consisting of distillers feed, fuel grade alcohol, and corn oil. Our principal ingredient solutions segment raw material is wheat flour, which is processed into starches and proteins. The cost of grain has at times been subject to substantial fluctuation.

In 2016, we purchased most of our grain requirements from two suppliers, Bunge Milling and Consolidated Grain and Barge ("CGB"). Our current grain supply contracts with Bunge Milling and CGB both expire December 31, 2017. These contracts permit us to purchase grain for delivery up to 12 months into the future at negotiated prices, based on a formula using several factors. We also order wheat flour anywhere from one to 24 months into the future. We provide for our wheat flour requirements through a supply contract with Ardent Mills, which has a term that expires July 10, 2019. We typically enter contracts for future delivery only to protect margins on contracted alcohol sales, expected ingredient sales, and general usage.

Our principal packaging material for our distillery products segment is oak barrels. Both new and used barrels are utilized for the aging of premium bourbon and rye whiskeys. We purchase oak barrels from multiple suppliers and some customers supply their own barrels.

We also source food grade alcohol from Illinois Corn Processing, LLC ("ICP"), our 30 percent owned joint venture. See additional information related to ICP in "Equity Method Investments" below, MD&A, and Note 3.

ENERGY

We use natural gas to operate boilers that we use to make steam heat. We procure natural gas for our facilities in the open market from various suppliers. We have a risk management program whereby we may purchase contracts for the delivery of natural gas in the future at predetermined prices or we can purchase futures contracts on the exchange. Depending on existing market conditions, in Atchison we have the ability to transport gas through a gas pipeline owned by a wholly-owned subsidiary. Historically, prices of natural gas have been higher in the late fall and winter months than during other periods.

EMPLOYEES

As of December 31, 2016, we had a total of 311 employees. A collective bargaining agreement covering 105 employees at the Atchison facility expires on August 31, 2019. Another collective bargaining agreement covering 60 employees at the Lawrenceburg facility expires on December 31, 2017. We consider our relations with our personnel generally to be good.

REGULATION

We are subject to a broad range of federal, state, local and foreign laws and regulations intended to protect public health and the environment. Our operations are also subject to regulation by various federal agencies, including the Alcohol and Tobacco Tax Trade Bureau ("TTB"), the Occupational Safety and Health Administration ("OSHA"), the Food and Drug Administration ("FDA") and the U.S. Environmental Protection Agency ("EPA"), and by various state and local authorities. Such regulations cover virtually every aspect of our operations, including production and storage facilities, marketing, pricing, labeling, packaging, advertising, water usage, waste water discharge, disposal of hazardous wastes and emissions and other matters.

TTB regulation includes periodic TTB audits of all production reports, shipping documents, and licenses to assure that proper records are maintained. We are also required to file and maintain monthly reports with the TTB of alcohol inventories and shipments.

EQUITY METHOD INVESTMENTS

Illinois Corn Processing, LLC ("ICP"). On November 20, 2009, we completed a series of related transactions pursuant to which we contributed our Pekin facility and certain maintenance and repair materials to a newly-formed company, ICP, and then sold 50 percent of the membership interest in ICP to ICP Holdings, an affiliate of SEACOR. ICP reactivated distillery operations at the Pekin facility during the quarter ended March 31, 2010, and now produces high quality food grade alcohol, chemical intermediates, and fuel.

In connection with these transactions, we entered into various agreements with ICP and ICP Holdings, including a Contribution Agreement, an LLC Interest Purchase Agreement and a Limited Liability Company Agreement. Under the LLC Interest Purchase Agreement, we sold ICP Holdings 50 percent of the membership interest in ICP. This agreement gave ICP Holdings the option to purchase up to an additional 20 percent of the membership interest in ICP at any time between the second and fifth anniversary based on agreed to criteria. On February 1, 2012, ICP Holdings exercised its option and purchased an additional 20 percent from us for $9,103, reducing our ownership from 50 percent to 30 percent.

Pursuant to the Limited Liability Company Agreement, control of day to day operations generally is retained by the members, acting by a majority in interest. Following ICP Holdings' exercise of its option referred to above, ICP Holdings owns 70 percent of ICP and generally is entitled to control its day to day operations. The Limited Liability Company Agreement also provides for the creation of an advisory board which consists of two advisers appointed by us and four advisers appointed by ICP Holdings. All actions of the advisory board require majority approval of the entire board, except that any transaction between ICP and ICP Holdings or its affiliates must be approved by the advisers appointed by us. The Limited Liability Company Agreement gives either member certain rights to shut down the facility if it operates at a loss. Such rights are conditional in certain instances but absolute if EBITDA (as defined in the agreement) losses are an aggregate $1,500 over any three consecutive quarters or if ICP's net working capital is less than $2,500. ICP Holdings also has the right to shut down the facility if ICP is in default under its loan agreement for failure to pay principal or interest for two months.

On April 9, 2015, ICP obtained a $30,000 revolving credit facility with JPMorgan Chase Bank, N.A., which may be increased in the future by an additional $20,000, subject to lender approval. The revolver matures on April 9, 2018. Simultaneous with the execution of the April 2015 revolving credit facility, ICP terminated its $15,000 amended and restated revolving credit facility with an affiliate of SEACOR, which would have matured January 31, 2016. We have no obligation to provide additional funding to ICP.

D.M. Ingredients GmbH ("DMI"). In 2007, we acquired a 50 percent interest in DMI, a German joint venture company that produces certain of our specialty ingredients products through a toller for distribution in the European Union ("E.U.") and elsewhere.

On December 29, 2014, we gave notice to D.M. Ingredients, GmbH, ("DMI") and to our partner in DMI, Crespel and Dieters GmbH & Co. KG ("C&D"), to terminate our joint venture effective June 30, 2015. C&D also provided notice to terminate DMI effective June 30, 2015. On June 22, 2015, a termination agreement was executed by and between us, DMI, and C&D to dissolve DMI effective June 30, 2015. On June 22, 2015 a termination agreement was executed by and between us and DMI to terminate our distribution agreement effective June 29, 2015. Under German law, commencing on June 30, 2015, normal operations for DMI ceased and a one year winding down process began once the registration of resolutions, appointment of liquidators, inventory count, and publication of the notice to potential creditors was complete, which occurred on October 29, 2015. On December 23, 2016, we received our portion of the remaining DMI liquidation proceeds, which totaled $351, as a return of our investment.

EXECUTIVE OFFICERS OF THE REGISTRANT

Our officers as of December 31, 2016 and their ages as of March 8, 2017 are listed below.

|

| | | |

Name | Age | Position | First elected to officer position |

Augustus C. Griffin | 57 | President and Chief Executive Officer | 2014 |

Thomas K. Pigott | 52 | Vice President, Finance and Chief Financial Officer | 2015 |

Stephen J. Glaser | 56 | Vice President, Production and Engineering | 2015 |

David E. Dykstra | 53 | Vice President, Alcohol Sales and Marketing | 2009 |

Michael R. Buttshaw | 54 | Vice President, Ingredient Sales and Marketing | 2014 |

David E. Rindom | 61 | Vice President and Chief Administrative Officer | 2000 |

Andrew P. Mansinne | 57 | Vice President, Brands | 2016 |

Mr. Griffin has served as President and Chief Executive Officer of MGP since July 2014 and as a member of the Board of Directors since August 2014. Prior to joining MGP, Mr. Griffin served from April 2013 to January 2014 as Executive Vice President of Marketing for Next Level Spirits, a northern California based producer, importer and distributor of premium wine and spirits brands. Between November 2011 and March 2013, he served as Brand and Business Consultant for Nelson’s Green Brier Distillery. From January 2008 to April 2011, Mr. Griffin was Senior Vice President, Global Managing Director of Brown Forman Corporation's flagship Jack Daniels business. Prior to 2008, he served for over 20 years in increasingly important brand management and general management leadership roles at Brown Forman.

Mr. Pigott has served as Vice President of Finance and Chief Financial Officer since September 2015. Prior to joining MGP, Mr. Pigott served in various Vice President roles with Kraft Foods Group. He was Vice President of Finance for the Meal Solutions Division from March 2015 to August 2015, Vice President of Finance for the Meals and Desserts Business Unit from May 2014 to March 2015, and Vice President of Finance and Chief Audit Executive from October 2012 to April 2014. From April 2010 to October 2012, Mr. Pigott was Vice President of Finance for the Pizza Division at Nestle, U.S.A., and from March 2010 to May 2010, he was Senior Director of Finance for the Pizza Division at Nestle, U.S.A. Prior to joining Nestle, between 1994 and 2010, Mr. Pigott held a succession of chief financial officer and other financial leadership positions across a wide number of operating divisions at Kraft Foods. His experience spans financial planning, analysis, audit and investor relations functions.

Mr. Glaser has served as Vice President of Production and Engineering at MGP since October 2015. Previously, he was Corporate Director of Operations since January 2014 and Plant Manager of the Company’s Atchison, Kansas, facility from May 2011 to December 2013. Prior to joining the Company, Mr. Glaser served for three years, from March 2008 to April 2011, as President and Chief Executive Officer of Briggs Industries, a leading, multi-site international kitchen and bath products business, following three years as Vice President of Operations for the company. Preceding his employment at Briggs, he held supply chain related positions with increased responsibility at Sony Electronics, Ingersoll Rand’s Schlage Lock Company, and Electrolux Home Products.

Mr. Dykstra has served as Vice President of Alcohol Sales and Marketing at MGP since 2009. He previously had been Industrial Alcohol Sales manager since 2006. He first joined the Company in 1988 eventually serving as Director of Sales for both beverage and fuel grade alcohol. In 1999, he left the Company to assume the role of Vice President of Sales and Marketing for Abengoa Bio Energy. He remained in that position until 2003, when he joined United Bio Energy Fuels, L.L.C. as Vice President of the alcohol marketing division. He returned to MGP in 2006.

Mr. Buttshaw has served as Vice President of Ingredients Sales and Marketing at MGP since December 2014. He previously served from October 2010 to November 2014 as Vice President of Sales for the ingredient group at Southeastern Mills, Inc. Just prior to that, Mr. Buttshaw was Vice President of Sales and Marketing for Penford Food Ingredients. This followed two years as Vice President of Sales and Business Development-specialty enzymes for DSM Food Specialties. From 1985 to 2008, Mr. Buttshaw was employed with Hormel Foods Corporation.

Mr. Rindom has served as Vice President and Chief Administrative Officer at MGP since December 2015. He previously served as the Company's Vice President, Human Resources since June 2000. Mr. Rindom was Corporate Director of Human Relations from 1992 to June 2000, Personnel Director from 1988 to 1992, and Assistant Personnel Director from 1984 to 1988 after his employment with the Company began in 1980.

Mr. Mansinne has served as Vice President of Brands since November 2016. Prior to joining the Company, Mr. Mansinne served as a managing director at Intercontinental Beverage Capital, as well as President of Tattico Strategies, in Bethesda, Maryland, from March 2015 through October 2016. Between May 2010 and April 2014, Mr. Mansinne was President of Aveniu Brands in Baltimore. He also served as Chief Executive Officer of DOmedia, Columbus, Ohio, from 2008 to 2010 following a year as Vice President of Marketing for Fosters Wine Estates, Napa, California. Mr. Mansinne served as a Senior Vice President at Brown-Forman Corporation, Louisville, Kentucky, where he began as Brand Director in 1995. Prior to 1995, Mr. Mansinne served in marketing and product management roles with other major consumer products companies, including The Quaker Oats Company, G. Heileman Brewing Company, and Ralston Purina Company.

ITEM 1A. RISK FACTORS

Our business is subject to certain risks and uncertainties. The following discussion identifies those which we consider to be most important. The following discussion of risks is not all inclusive. Additional risks not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition, or results of operations.

RISKS THAT AFFECT OUR BUSINESS AS A WHOLE

An interruption of operations, a catastrophic event at our facilities, or a disruption of transportation services could negatively affect our business.

Although we maintain insurance coverage for various property damage and loss events, an interruption in or loss of operations at either of our facilities, or the facilities of ICP, could reduce or postpone production of our products, which could have a material adverse effect on our business, results of operations and/or financial condition. To the extent that our value added products rely on unique or proprietary processes or techniques, replacing lost production by purchasing from outside suppliers becomes more difficult.

Our customers store a substantial amount of barreled inventory of aged premium bourbon and rye whiskeys at our Lawrenceburg facility. If there was a catastrophic event at our Lawrenceburg facility, our customers' business could be adversely affected. The loss of a significant amount of aged inventory through fire, natural disaster, or otherwise could result in a significant reduction in supply of the affected product or products and, if we are negligent in the custodial care of our customers' inventory, this could result in customer claims against us.

We also store a substantial amount of our own inventory of aged premium bourbon and rye whiskeys at our Lawrenceburg facility. If there was a catastrophic event at our Lawrenceburg facility, our business could be adversely affected. The loss of a significant amount of our aged inventory through fire, natural disaster, or otherwise could result in a reduction in supply of the affected product or products and could affect our long-term growth.

A disruption in transportation services could result in difficulties supplying materials to our facilities and impact our ability to deliver products to our customers in a timely manner.

Our profitability is affected by the costs of energy, grain, and wheat flour that we use in our business, the availability and cost of which are subject to weather and other factors beyond our control. We may not be able to recover the costs of commodities and energy by increasing our selling prices.

Grain and wheat flour costs are a significant portion of our costs of goods sold. Historically, the cost of such raw materials has been subject to substantial fluctuation, depending upon a number of factors which affect commodity prices in general and over which we have no control. These include crop conditions, weather, disease, plantings, government programs and policies, competition for acquisition of inputs such as agricultural commodities, purchases by foreign governments, and changes in demand resulting from population growth and customer preferences. The price of natural gas also fluctuates based on anticipated changes in supply and demand, weather and the prices of alternative fuels. Fluctuations in the price of commodities and natural gas can be sudden and volatile at times and have had, from time to time, significant adverse effects on the results of our operations. Higher energy costs could result in higher transportation costs and other operating costs.

We do not enter into futures and options contracts because we can purchase grain and wheat flour for delivery up to 12 months into the future under our grain supply agreements. We intend to contract for the future delivery of grain and wheat flour, only to protect margins on expected sales. On the portion of volume not hedged, we will attempt to recover higher commodity costs through higher selling prices, but market considerations may not always permit this. Even where prices can be adjusted, there would likely be a lag between when we experience higher commodity or natural gas costs and when we might be able to increase prices. To the extent we are unable to timely pass increases in the cost of raw materials to our customers under sales contracts, market fluctuations in the cost of grain, natural gas and ethanol may have a material adverse effect on our results of operations and financial condition.

We source our grain and wheat flour from a limited number of suppliers.

We have signed supply agreements with Bunge Milling and CGB for our grain supply (primarily corn) and Ardent Mills for our wheat flour. If any of these companies encounters an operational or financial issue, or otherwise cannot meet our supply demands, it could lead to an interruption in supply to us and/or higher prices than those we have negotiated or than are available in the market at the time.

Risks related to our 30 percent equity method investment in ICP:

ICP, like many others in the ethanol industry, in 2014 experienced high levels of profitability, resulting in a disproportionate share of our improvement in net income for the year ended December 31, 2014, and those levels may not recur. Because of ICP's strong financial performance, ICP was able to distribute cash to us, but this may not recur.

Our proportionate share of the profits of ICP has in the recent past had a significant positive impact on our net income. The earnings performance in 2014 was due to strong margins in the production of chemical intermediates and high quality alcohol. The margins were driven primarily by a low current supply and strong demand for these products and for fuel grade alcohol, which affected their pricing. From 2014 to 2015, while ICP experienced lower sales volumes and a lower average per unit selling price, our proportionate share of the earnings of ICP results continued to have a positive impact on our earnings. From 2015 to 2016, while ICP has experienced higher sales volumes, per unit average selling prices were lower, reflective of less favorable market conditions than recent years and resulting in a lower positive impact to our earnings. We currently expect that ICP's recent levels of profitability may not be sustained and, as a consequence, that ICP's contributions to our future net income may be reduced.

On December 4, 2014, we received a $4,835 cash dividend distribution from ICP. On February 26, 2016, we received a second cash dividend distribution from ICP in the amount of $3,300, which was our 30 percent ownership share of the total distribution (see Notes 3 and 14). There is no assurance cash dividend distributions will be received from ICP in the future.

We have a minority interest in ICP, which limits our ability to influence ICP's operations and profitability.

We have a minority interest in ICP of 30 percent, and have only two representatives on the six member Advisory Board of ICP. Our minority ownership position and limited advisory role mean that our ability to influence operating decisions and affect profitability of the joint venture is limited. We do not control ICP's operations, strategies, or financial decisions. The majority equity owner may have economic, business or legal interests that are inconsistent with our goals or the goals we would set for ICP. We are dependent on the management of ICP and the other members of the Advisory Board to operate the joint venture profitably and take our interests into account. We must rely on others to implement beneficial management strategies, including appropriate risk management, internal controls over financial reporting, and compliance monitoring. The ICP Limited Liability Company Agreement generally allocates the profits, losses and distributions of cash of ICP based on our percentage membership interest in ICP, which is derived from our capital contributions to ICP relative to the total contributions to ICP from all members. Our proportionate share of the earnings and losses are reflected in our financial statements. Any cash distributions from ICP (other than certain mandatory distributions for tax liabilities) must be approved by the Advisory Board, which we do not control.

Our ability to supply our industrial alcohol business is highly dependent on sourcing the product from ICP or unaffiliated third parties.

ICP has been an important source of industrial alcohol in the past and we expect this to continue into the foreseeable future along with other third party sources. While we plan to continue to source industrial alcohol from ICP in 2017, ICP is under no obligation to sell to us. If we are unsuccessful in sourcing product from ICP or other sources, our ability to supply our industrial alcohol business at current levels could be impacted.

We have incurred impairment and restructuring charges in the past and may suffer such charges in the future.

We review long-lived assets and goodwill for impairment at year end or if events or circumstances indicate that usage may be limited and carrying values may not be recoverable. Should events indicate that assets cannot be used as planned, the realization from alternative uses or disposal is compared to their carrying value. If an impairment loss is measured, this estimate is recognized and affects our profitability. Considerable judgment is used in these measurements, and a change in the assumptions could result in a different determination of impairment loss and/or the amount of any impairment.

The markets for our products are very competitive, and our results could be adversely affected if we do not compete effectively.

The markets for products in which we participate are very competitive. Our principal competitors in these markets have substantial financial, marketing and other resources, and several are much larger enterprises than us.

We are dependent on being able to generate net sales and other operating income in excess of cost of products sold in order to obtain margins, profits and cash flows to meet or exceed our targeted financial performance measures. Competition is based on such factors as product innovation, product characteristics, product quality, pricing, color and name. Pricing of our products is partly dependent upon industry processing capacity, which is impacted by competitor actions to bring online idled capacity or to build new production capacity. If market conditions make our products too expensive for use in consumer goods, our revenues could be affected. If our principal competitors were to decrease their pricing, we could choose to do the same, which could adversely affect our margins and profitability. If we did not do the same, our revenues could be adversely affected due to the potential loss of sales or market share. Our revenue growth could also be adversely affected if we are not successful in developing new products for our customers or as a result of new product introductions by our competitors. In addition, more stringent new customer demands may require us to make internal investments to achieve or sustain competitive advantage and meet customer expectations.

Unsuccessful research activities or product launches could affect our profitability.

Research activities and product launch activities are inherently uncertain. The failure to launch a new product successfully can give rise to inventory write offs and other costs and can affect consumer perception of an existing brand. Any significant changes in consumer preferences and failure to anticipate and react to such changes could result in reduced demand for our products. If we were to have unsuccessful research activities or product launches, our profitability could be affected.

Work disruptions or stoppages by our unionized workforce could cause interruptions in our operations.

As of December 31, 2016, approximately 165 of our 311 employees were members of a union. Although our relations with our two unions are stable and our labor contracts do not expire until December 2017 and August 2019, there is no assurance that we will not experience work disruptions or stoppages in the future, which could have a material adverse effect on our business and results of operations and could adversely affect our relationships with our customers.

If we were to lose any of our key management personnel, we may not be able to fully implement our strategic plan, our system of internal controls could be impacted, and our operating results could be adversely affected.

We rely on the continued services of key personnel involved in management, finance, product development, sales, manufacturing and distribution, and, in particular, upon the efforts and abilities of our executive management team. The loss of service of any of our key personnel could have a material adverse effect on our business, financial condition, results of operations, and on our system of internal controls.

If we cannot attract and retain key management personnel, or if our search for qualified personnel is prolonged, our system of internal controls may be affected, which could lead to an adverse effect on our operating results. In addition, it could be difficult, time consuming and expensive to replace any key management member or other critical personnel, and no guarantee exists that we will be able to recruit suitable replacements or assimilate new key management personnel into our organization.

Covenants and other provisions in our credit facility could hinder our ability to operate. Our failure to comply with covenants in our credit facility could result in the acceleration of the debt extended under such facility, limit our liquidity, and trigger other rights of our lenders.

Our credit agreement contains a number of financial and other covenants that include provisions which require us, in certain circumstances, to meet certain financial tests. These covenants could hinder our ability to operate and could reduce our profitability. In addition, our credit agreement permits the lender to modify borrowing base and advance rates, the effect of which may limit our available credit under the agreement. The lender may also terminate or accelerate our obligations under the credit agreement upon the occurrence of various events in addition to payment defaults and other breaches. Any acceleration of our debt, modification to reduce our borrowing base, or termination of our credit agreement would negatively impact our overall liquidity and may require us to take other actions to preserve any remaining liquidity. Although we anticipate that we will be able to meet the covenants in our credit agreement, there can be no assurance that we will do so, as there are a number of external factors that affect our operations over which we have little or no control.

Product recalls or other product liability claims could materially and adversely affect us.

Selling products for human consumption involves inherent legal and other risks, including product contamination, spoilage, product tampering, allergens, or other adulteration. We could decide to, or be required to, recall products due to suspected or confirmed product contamination, adulteration, misbranding, tampering, or other deficiencies. Although we maintain product recall insurance, product recalls or market withdrawals could result in significant losses due to their costs, the destruction of product inventory, and lost sales due to the unavailability of the product for a period of time. We could be adversely affected if our customers lose confidence in the safety and quality of certain of our products, or if consumers lose confidence in the food and beverage safety system generally. Adverse attention about these types of concerns, whether or not valid, may damage our reputation, discourage consumers from buying our products, or cause production and delivery disruptions.

We may also suffer losses if our products or operations cause injury, illness, or death. In addition, our marketing could face claims of false or deceptive advertising or other criticism. A significant product liability or other legal judgment or a related regulatory enforcement action against us, or a significant product recall, may materially and adversely affect our reputation and profitability. Moreover, even if a product liability or other legal or regulatory claim is unsuccessful, has no merit, or is not pursued, the negative publicity surrounding assertions against our products or processes could materially and adversely affect our product sales, financial condition, and operating results.

We are subject to extensive regulation and taxation, and compliance with existing or future laws and regulations, which may require us to incur substantial expenditures.

We are subject to a broad range of federal, state, local and foreign laws and regulations relating to the protection of the public health and the environment. Our operations are also subject to regulation by various federal agencies, including the TTB, OSHA, the FDA, and the EPA, and by various state and local authorities. Such regulations cover virtually every aspect of our operations, including production and storage facilities, importing ingredients, distribution of beverage alcohol products, marketing, pricing, labeling, packaging, advertising, water usage, waste water discharge, disposal of hazardous wastes and emissions and other matters.

Violations of any of these laws and regulations may result in administrative, civil or criminal fines or penalties being levied against us, including temporary or prolonged cessation of production, revocation or modification of permits, performance of environmental investigatory or remedial activities, voluntary or involuntary product recalls, or a cease and desist order against operations that are not in compliance. These laws and regulations may change in the future and we may incur material costs in our efforts to comply with current or future laws and regulations. These matters may have a material adverse effect on our business and financial results.

A failure of one or more of our key information technology systems, networks, processes, associated sites, or service providers could have a material adverse impact on our business.

We rely on information technology ("IT") systems, networks, and services, including internet sites, data hosting and processing facilities and tools, hardware (including laptops and mobile devices), software and technical applications and platforms, some of which are managed and hosted by third party vendors to assist us in the management of our business. The various uses of these IT systems, networks, and services include, but are not limited to: hosting our internal network and communication systems; enterprise resource planning; processing transactions; summarizing and reporting results of operations; business plans, and financial information; complying with regulatory, legal, or tax requirements; providing data security; and handling other processes necessary to manage our business. Although we have an offsite backup system and disaster recovery plan, any failure of our information systems could adversely impact our ability to operate. Routine maintenance or development of new information systems may result in systems failures, which may adversely affect our business, results of operations and financial results.

Increased IT security threats and more sophisticated cyber crime pose a potential risk to the security of our IT systems, networks, and services, as well as the confidentiality, availability, and integrity of our data. This can lead to outside parties having access to our privileged data or strategic information, our employees or our customers. Any breach of our data security systems or failure of our information systems may have a material adverse impact on our business operations and financial results. If the IT systems, networks, or service providers we rely upon fail to function properly, or if we suffer a loss or disclosure of business or other sensitive information, due to any number of causes, ranging from catastrophic events to power outages to security breaches, and our disaster recovery plans do not effectively address these failures on a timely basis, we may suffer interruptions in our ability to manage operations and reputational, competitive, or business harm, which may adversely affect our business operations or financial condition. In addition, such events could result in unauthorized disclosure of material confidential information, and we may suffer financial and reputational damage because of lost or misappropriated confidential information belonging to us or to our partners, our employees, customers, and suppliers. Although we maintain insurance coverage for various cybersecurity risks, in any of these events, we could also be required to spend significant financial and other resources to remedy the damage caused by a security breach or to repair or replace networks and IT systems.

Damage to our reputation, or that of any of our key customers or their brands, could affect our stock price and business performance.

The success of our products depends upon the positive image that consumers have of the third party brands that use our products. Contamination, whether arising accidentally or through deliberate third party action, or other events that harm the integrity or consumer support for our and/or our customers' products and could affect the demand for our and/or our customers' products. Unfavorable media, whether accurate or not, related to our industry or to us or our products, or to the brands that use our products, marketing, personnel, operations, business performance or prospects could negatively affect our corporate reputation, stock price, ability to attract high quality talent or the performance of our business. Adverse publicity or negative commentary on social media outlets could cause consumers to react rapidly by avoiding our brands or choosing brands offered by our competitors, which could materially negatively affect our financial results, business and financial condition.

RISKS SPECIFIC TO OUR DISTILLERY PRODUCTS SEGMENT

The relationship between the price we pay for grain and the sales prices of our distillery co-products can fluctuate significantly and affect our results of operations.

Distillers feed, fuel grade alcohol, and corn oil are the principal co-products of our alcohol production process and can contribute in varying degrees to the profitability of our distillery products segment. Distillers feed and corn oil are sold for prices which historically have tracked the price of corn, but, certain of our co-products compete with similar products made from other plant feedstocks, the cost of which may not have risen in unison with corn prices. We sell fuel grade alcohol, the prices for which typically, but not always, have tracked price fluctuations in gasoline prices. As a result, the profitability of these products could be affected.

Our strategic plan involves significant investment in the aging of barreled distillate. Decisions concerning the quantity of maturing stock of our aged distillate could affect our future profitability.

There is an inherent risk in determining the quantity of maturing stock of aged distillate to lay down in a given year for future sales as a result of changes in consumer demand, pricing, new brand launches, changes in product cycles, and other factors. Demand for products can change significantly between the time of production and the date of sale. It may be more difficult to make accurate prediction regarding new products and brands. Inaccurate decisions and/or estimations could lead to an inability to supply future demand or lead to a future surplus of inventory and consequent write down in the value of maturing stocks of aged distillate. As a result, profitability of the distillery products segment could be affected.

If the brands we develop or acquire do not achieve consumer acceptance, our growth may be limited, which could have a material adverse impact on our operating results.

A component of our strategic plan is to develop our own brands, particularly whiskeys. Risks related to this strategy include:

| |

• | Because our brands, internally developed and acquired, are early in their growth cycle or have not yet been developed, they have not achieved extensive brand recognition. Accordingly, if consumers do not accept our brands, we will not be able to penetrate our markets and our growth may be limited. |

| |

• | We depend, in part, on the marketing initiatives and efforts of our independent distributors in promoting our products and creating consumer demand and we have limited or no control regarding their promotional initiatives or the success of their efforts. |

| |

• | We depend on our independent distributors to distribute our products. The failure or inability of even a few of our independent distributors to adequately distribute our products within their territories could harm our sales and result in a decline in our results of operations. |

| |

• | We compete for shelf space in retail stores and for marketing focus by our independent distributors, most of whom carry extensive product portfolios. |

| |

• | The laws and regulations of several states prohibit changes of independent distributors, except under certain limited circumstances, making it difficult to terminate an independent distributor for poor performance without reasonable cause, as defined by applicable statutes. Any difficulty or inability to replace independent distributors, poor performance of our major independent distributors or our inability to collect accounts receivable from our major independent distributors could harm our business. There can be no assurance that the independent distributors and retailers we use will continue to purchase our products or provide our products with adequate levels of promotional support. |

Warehouse expansion issues could affect our operations and/or adversely affect our financial results.

On October 21, 2015, we announced a major expansion in warehousing capacity on a 20-acre campus adjoining the Company's current Lawrenceburg facility. Our Board of Directors has approved additional investments for the project, for a total approved investment of $29,000. The program includes both the refurbishment of existing warehouse buildings and the construction of new warehouses. The first projects included in this program were completed in late 2015, with additional projects completed in 2016. Additional warehouse capacity included in the total approved program is expected to be completed by the end of 2018. There is the potential risk of completion delays, including risk of delay associated with required permits, and cost overruns, which could affect our business, financial condition and results of operations.

Water scarcity or quality could negatively impact our production costs and capacity.

Water is the main ingredient in substantially all of our distillery products. It is also a limited resource, facing unprecedented challenges from climate change, increasing pollution, and poor management. As demand for water continues to increase, water becomes more scarce and the quality of available water deteriorates, we may be affected by increasing production costs or capacity constraints, which could adversely affect our results of operations, business and financial results.

We may be subject to litigation directed at the beverage alcohol industry.

Companies in the beverage alcohol industry are, from time to time, exposed to class action or other litigation relating to alcohol advertising, product liability, alcohol abuse problems or health consequences from the misuse of alcohol. Such litigation may result in damages, penalties or fines as well as damage to our reputation, which could have a material adverse effect on our cash flows, financial condition and financial results.

Adverse public opinion about alcohol could reduce demand for our products.

In recent years, there has been increased social and political attention directed at the beverage alcohol industry. The recent attention has focused largely on public health concerns related to alcohol abuse, including drunk driving, underage drinking, and the negative health impacts of the abuse and misuse of beverage alcohol.

Anti-alcohol groups have, in the past, advocated successfully for more stringent labeling requirements, higher taxes and other regulations designed to discourage alcohol consumption. More restrictive regulations, higher taxes, negative publicity regarding alcohol consumption and/or changes in consumer perceptions of the relative healthfulness or safety of beverage alcohol could decrease sales and consumption of alcohol and thus the demand for our products. This could, in turn, significantly decrease both our revenues and our revenue growth and have a material adverse effect on our results of operations, business and financial results.

RISKS SPECIFIC TO OUR INGREDIENT SOLUTIONS SEGMENT

Our focus on higher margin specialty ingredients may make us more reliant on fewer, more profitable customer relationships.

Our strategic plan for our ingredient solutions segment includes focusing our efforts on the sale of specialty proteins and starches to targeted domestic consumer packaged goods customers. Our major focus is directed at food ingredients, which are primarily used in foods that are developed to address consumers’ desire for healthier and more convenient products; these consist of dietary fiber, wheat protein isolates and concentrates and textured wheat proteins. The bulk of our applications technology and research and development efforts are dedicated to providing customers with specialty ingredient solutions that deliver nutritional benefits, as well as desired functional and sensory qualities to their products. Our business and financial results could be materially adversely affected if our customers were to reduce their new product development ("NPD") activities or cease using our unique dietary fibers, starches and proteins in their NPD efforts.

Products competing with our Fibersym® resistant starch could lead to a decrease in sales volume or pricing, a decrease in margins and lower profitability.

Our patent rights to Fibersym® expire in 2017. We face competition with our Fibersym® resistant starch. The competition could lead to diminished returns and lower our margins. This factor could result in significant costs and could have a material adverse effect on our business, cash flows and financial results.

In November 2016, we announced that we filed a citizen petition with the FDA asking the agency to further confirm the status of our patented Fibersym® RW and FiberRite® RW resistant wheat starches as dietary fiber. A list of dietary fibers is currently being developed by the FDA under new food labeling rules, which were published on May 27, 2016 and have a scheduled compliance date of July 26, 2018. While our citizen petition is undergoing review, the current status of Fibersym® RW, along with FiberRite® RW, as accepted dietary fiber and a recognized fiber fortifying ingredient remains in place. A delay in confirmation by the FDA of our patented Fibersym® RW and FiberRite® RW resistant wheat starches as dietary fiber under the new food labeling rules in a timely manner could have a material adverse impact on ingredient solutions segment operating results.

Adverse public opinion about any of our specialty ingredients could reduce demand for our products.

Consumer preferences with respect to our specialty ingredients might change. In fact, in recent years, we have noticed shifting consumer preferences and media attention directed to gluten, gluten intolerance, and "clean label" products. Shifting consumer preferences could decrease demand for our specialty ingredients. This could, in turn, significantly decrease our revenues and revenue growth, which could have a material adverse affect on our cash flows, financial condition and financial results.

RISKS RELATED TO OUR COMMON STOCK

Common Stockholders have limited rights under our Articles of Incorporation.

Under our Articles of Incorporation, holders of our Preferred Stock are entitled to elect five of our nine directors and only holders of our Preferred Stock are entitled to vote with respect to a merger, dissolution, lease, exchange or sale of substantially all of our assets, or on an amendment to the Articles of Incorporation, unless such action would increase or decrease the authorized shares or par value of the Common or Preferred Stock, or change the powers, preferences or special rights of the Common or Preferred Stock so as to affect the holders of Common Stock adversely. Generally, the Common Stock and Preferred Stock vote as separate classes on all other matters requiring stockholder approval.

The majority of the outstanding shares of our Preferred Stock is beneficially owned by one individual, who is effectively in control of the election of five of our nine directors under our Articles of Incorporation.

The trading volume in our Common Stock fluctuates depending on market conditions. The sale of a substantial number of shares in the public market could depress the price of our stock and make it difficult for stockholders to sell their shares.

Our Common Stock is listed on the NASDAQ Stock Market. Our public float at December 31, 2016 was approximately 12,712,845 shares, as approximately 3,945,920 shares are held by affiliates. Over the year ended December 31, 2016, our daily trading volume as reported to us by NASDAQ has fluctuated from 31,600 to 3,103,500 shares (excluding block trades). When trading volumes are relatively light, significant price changes can occur even when a relatively small number of shares are being traded and an investor’s ability to quickly sell quantities of stock may be affected.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

MGP has two primary locations: Atchison, Kansas and Lawrenceburg and Greendale, Indiana. Grain processing, distillery, warehousing, research and quality control laboratories, principal executive office building and the technical innovation center are located in Atchison, Kansas on a 28.5 acre campus. A distillery, warehousing, tank farm, quality control, and research and development facilities are located in Lawrenceburg and Greendale, Indiana on a 78 acre campus.

These facilities are generally in good operating condition, and are generally suitable for the business activity conducted therein. We have existing manufacturing capacity to grow our ingredient solutions business at our Atchison facility, as needed. All of our production facilities, executive office building, and technical innovation center are owned and all of our owned properties are subject to mortgages in favor of one or more of our lenders. We also own or lease transportation equipment and facilities and a gas pipeline as described under Item 1. Business - Transportation and Item 1. Business - Energy.

ITEM 3. LEGAL PROCEEDINGS

On December 21, 2016, the U.S. Environmental Protection Agency (“EPA”) issued a Notice of Violation to the Company alleging the Company commenced construction of new aging warehouses for whiskey at its facility in Lawrenceburg, Indiana, without first applying for or obtaining a Clean Air Act permit and without adequately demonstrating to the EPA that emissions control equipment did not need to be installed to meet applicable air quality standards. The Company notes that neither EPA nor the State of Indiana have required emission control equipment for aging whiskey warehouses and, to our knowledge, no other distillers in the U.S. have been required to install emissions control equipment in their aging whiskey warehouses. No demand for a penalty has been made in connection with the Notice of Violation, but the Company believes it is probable that a penalty will be assessed. Although it is not possible to reasonably estimate a loss or range of loss at the date of this filing, the Company currently does not expect that the amount of any such penalty or related remedies would have a material adverse effect on the Company’s business, financial condition or results of operations.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDERS MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Equity compensation plans’ information is incorporated by reference from Part III, Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters,” of this document, should be considered an integral part of Item 5. Our Common Stock is traded on the NASDAQ Global Select Market. At March 3, 2017, there were approximately 533 holders of record of our Common Stock. According to reports received from NASDAQ, the average daily trading volume of our Common Stock (excluding block trades) ranged from 31,600 to 3,103,500 shares during the year ended December 31, 2016.

HISTORICAL STOCK PRICES AND DIVIDENDS

The table below reflects the high and low sales prices of our Common Stock and the details of dividends and dividend equivalents per share for each quarter of 2016 and 2015:

|

| | | | | | | | | | | | | | | |

| Stock Sales Price | | Dividend and Dividend Equivalent Information (per Share and Unit) |

| High | | Low | | Declared | | Paid |

2016 | | | | | | | |

First Quarter | $ | 26.52 |

| | $ | 19.91 |

| | $ | 0.08 |

| | $ | — |

|

Second Quarter | 39.50 |

| | 22.11 |

| | — |

| | 0.08 |

|

Third Quarter | 44.25 |

| | 33.38 |

| | 0.02 |

| | 0.02 |

|

Fourth Quarter | 53.22 |

| | 31.93 |

| | 0.02 |

| | 0.02 |

|

| |

| | |

| | $ | 0.12 |

| | $ | 0.12 |

|

2015 | | | | | | | |

First Quarter | $ | 16.71 |

| | $ | 13.06 |

| | $ | 0.06 |

| | $ | — |

|

Second Quarter | 19.22 |

| | 12.32 |

| | — |

| | 0.06 |

|

Third Quarter | 17.31 |

| | 12.85 |

| | — |

| | — |

|

Fourth Quarter | 27.56 |

| | 15.56 |

| | — |

| | — |

|

| | | | | $ | 0.06 |

| | $ | 0.06 |

|

Our credit agreement (the "Credit Agreement") with Wells Fargo Bank allows for the payment of cash dividends (as defined in Restricted Payments of the Credit Agreement), which are limited to $2,000. Restricted Payments are allowed to exceed $2,000 provided we maintain Excess Availability of 17.5 percent of the Total Facility Amount and a Fixed Charge Coverage Ratio for the most recently completed 12 months of at least 1.10:1.00, or if Excess Availability exceeds 25 percent of the Total Facility Amount (with the terms "Restricted Payments," "Excess Availability," "Total Facility Amount," and "Fixed Charge Coverage Ratio" as defined in the Credit Agreement).

On February 15, 2017, the Board of Directors declared a quarterly dividend payable to stockholders of record as of March 1, 2017, of our Common Stock and a dividend equivalent payable to holders of RSUs as of March 1, 2017, of $0.04 per share and per unit. The dividend payment and dividend equivalent payment will occur on March 24, 2017.

We expect to continue our policy of paying quarterly cash dividends, although there is no assurance as to the declaration or amount of any future dividends because they are dependent on future earnings, capital requirements, and debt service obligations.

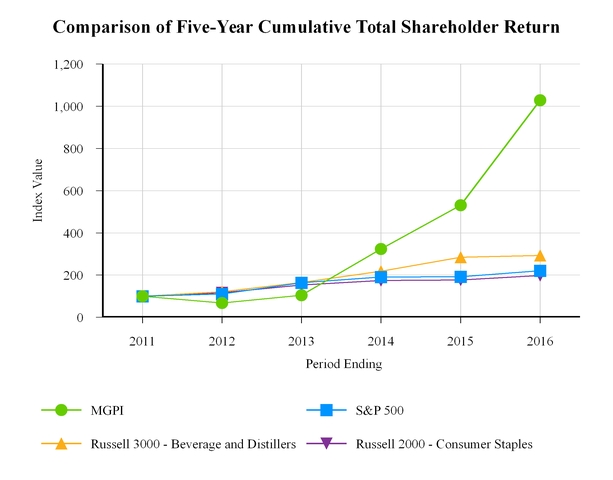

STOCK PERFORMANCE GRAPH

The following graph compares the cumulative total return of our Common Stock for the five year period ended December 31, 2016, against the cumulative total return of the S&P 500 Stock Index (broad market comparison), Russell 3000 - Beverage and Distillers (line of business comparison), and Russell 2000 - Consumer Staples (line of business comparison). The graph assumes $100 (one hundred dollars) was invested on December 31, 2011, and that all dividends were reinvested.

PURCHASES OF EQUITY SECURITIES BY ISSUER

We did not sell equity securities during the quarter ended December 31, 2016.

Issuer Purchases of Equity Securities

|

| | | | | | | | | | | | | | |

| | (a) Total Number of Shares (or Units) Purchased | | | (b) Average Price Paid per Share (or Unit) | | | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs |

October 1, 2016 through October 31, 2016 | | — |

| | | — |

| | | — |

| | — |

|

November 1, 2016 through November 30, 2016 | | — |

| | | — |

| | | — |

| | — |

|

December 1, 2016 through December 31, 2016 | | — |

| | | — |

| | | — |

| | — |

|

Total | | — |

| | | | | | — |

| | |

ITEM 6. SELECTED FINANCIAL DATA AND SUPPLEMENTARY FINANCIAL INFORMATION |

| | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2016(a)(h)(i) | | 2015(a) | | 2014(a),(b) | | 2013(c) | | 2012(d) |

Consolidated Statements of Income Data: | | | | | | | | | |

Net sales | $ | 318,263 |

| | $ | 327,604 |

| | $ | 313,403 |

| | $ | 323,264 |

| | $ | 334,335 |

|

Income before income taxes(e) | $ | 44,717 |

| | $ | 38,418 |

| | $ | 25,940 |

| | $ | (6,521 | ) | | $ | 1,942 |

|

Net income (loss) | $ | 31,184 |

| | $ | 26,191 |

| | $ | 23,675 |

| | $ | (4,929 | ) | | $ | 1,624 |

|

| | | | | | | | | |

Basic and Diluted Earnings (Loss) Per Share ("EPS") | | | | | | | | | |

Income (loss) from continuing operations | $ | 1.82 |

| | $ | 1.48 |

| | $ | 1.32 |

| | $ | (0.34 | ) | | $ | 0.09 |

|

Income from discontinued operations | — |

| | — |

| | — |

| | 0.05 |

| | — |

|

Net income (loss) | $ | 1.82 |

| | $ | 1.48 |

| | $ | 1.32 |

| | $ | (0.29 | ) | | $ | 0.09 |

|

| | | | | | | | | |

Cash dividends per common share | $ | 0.12 |

| | $ | 0.06 |

| | $ | 0.05 |

| | $ | 0.05 |

| | $ | 0.05 |

|

Consolidated Balance Sheet Data: | | | | | | | | | |

Total assets(f) | $ | 225,336 |

| | $ | 194,310 |

| | $ | 160,215 |

| | $ | 151,329 |

| | $ | 163,171 |

|

Long-term debt, less current maturities(f)(g) | 31,642 |

| | $ | 30,115 |

| | $ | 7,286 |

| | $ | 21,611 |

| | $ | 31,061 |

|

| |

(a) | During 2016, 2015 and 2014, we determined that we would more likely than not realize a portion of our deferred tax asset and reduced the valuation allowance by $718, $2,385, and $7,446, respectively. The 2014 reduction amount included an adjustment to other comprehensive loss of $172. |

| |

(b) | In January 2014 and October 2014, we experienced a fire at one of our facilities. Insurance recoveries totaled $8,290 for 2014. |

| |

(c) | In connection with the proxy contest related to our 2013 Annual Meeting of stockholders, we were involved in various proceedings with respect to MGP Ingredients, Inc. Voting Trust, the 2013 Annual Meeting and the Special Committee of the Board of Directors and incurred $5,465 of expenses in 2013. |

| |

(d) | Net income for 2012 includes a $4,055 gain related to the sale of a 20 percent interest in our joint venture, ICP. |

| |

(e) | For 2013, we reported discontinued operations. Accordingly, the caption for 2013 was Loss from continuing operations before income taxes. |

| |

(f) | In November 2015, the FASB issued ASU 2015-17, Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes. The ASU was effective for public business entities for interim and annual periods in fiscal years beginning after December 15, 2016. The intent of the new standard was to simplify reporting of deferred taxes. As such, the standard allows netting of current and non-current deferred taxes within a reporting jurisdiction and the resulting deferred tax assets and liabilities are presented as non-current in our Consolidated Balance Sheets at December 31, 2016 and 2015 since we elected to early adopt the ASU on a prospective basis. The balance sheet classifications for years ended December 31, 2014, 2013, and 2012 were not adjusted to be consistent with 2016 and 2015 reporting. |

| |

(g) | In April 2015, the FASB issued ASU No. 2015-03, Interest - Imputation of Interest (Subtopic 835-30), which requires that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. Our consolidated balance sheets have been adjusted and retrospectively adjusted at December 31, 2015 and 2014, respectively, for the presentation of debt issuance costs as required by ASU 2015-03. As of December 31, 2016, 2015, and 2014, we had $576, $636, and $384, respectively, of unamortized loan fees related to our debt that was reclassified as a direct deduction from the carrying amount of the related debt liability in the consolidated balance sheets. Years ended December 31, 2013 and 2012 were not adjusted to be consistent with 2016, 2015, and 2014 reporting. |

| |

(h) | In March 2016, the FASB issued ASU No. 2016-09, Compensation—Stock Compensation (Topic 718) Improvements to Employee Share-Based Payment Accounting. We elected to early adopt the accounting update in the quarter ended September 30, 2016 and, due to a required change in accounting principle required by the ASU adoption and the vesting of 128,500 shares of restricted stock during the quarter of adoption, we received a combined federal and state tax effected excess tax benefit of $1,571 from windfalls related to employee share-based compensation that was recognized as a reduction to income tax expense. Years ended December 31, 2015, 2014, 2013, and 2012 were not adjusted to be consistent with 2016 reporting. |

| |

(i) | Net income for 2016 included a legal settlement agreement and a gain on sale of long-lived assets totaling $3,385. |

Selected Financial Information

Selected quarterly financial information is detailed in Note 15.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS